In a move cited as ‘unexpected’ and ‘unprecedented’, the French government in March introduced a soft tax on palm oil which surprised many industry players and local authorities.

In a move cited as ‘unexpected’ and ‘unprecedented’, the French government in March introduced a soft tax on palm oil which surprised many industry players and local authorities.

The move has been seen as an “obstacle” to encourage and promote the usage of olive oil in the European Union (EU), thus creating an increased ‘burden’ to palm oil players to export their palm oil into European countries.

While the move has been viewed as a temporary setback, the stronger-than-expected dry season caused by the El Nino has proved to be a blessing in disguise for the plantation industry.

Market observers and analysts opined that the prolonged dry season caused by the El Nino has brought a sudden ‘wind of change’ for the industry.

They believed plantation players could benefit from the tailwinds by selling their crude palm oil (CPO) to ride on positive sentiment

In fact, analysts covering the plantation sector turned bullish on the sector back in October last year when the dry season lasted longer than usual.

They were among one of the first in upgrading the call for the plantation sector citing strong El Nino as the potential ‘catalyst’ that could provide a recovery for the CPO price.

While the effect of production and inventories have yet to be significant at that time, it was the early sign that pointed to a potential recovery of the CPO price.

RHB Research Institute Sdn Bhd (RHB Research) in a few reports last October has upgraded its CPO price assumption higher on strong El Nino situation.

The research firm believed the latest El Nino’s impact on edible oil supply will be one of the largest ever given that the phenomenon could match the one that happened in 1997-1998.

It also expects palm oil production to decline then while highlighted that CPO price could rally this year.

Lowest output in nine years

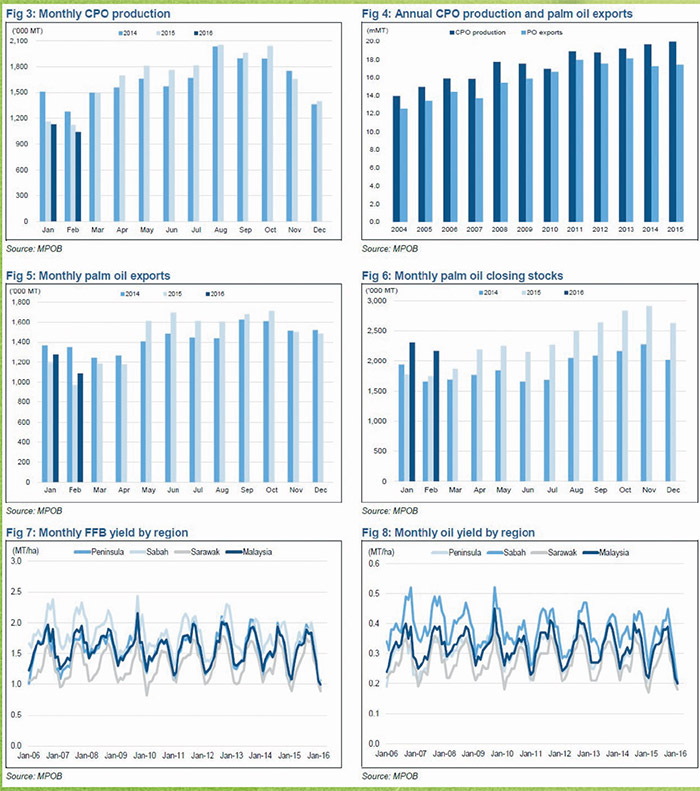

CPO production of 1.04 million metric tonnes (MT) recorded in February 2016 was the lowest output level seen since February 2007.

The production figure represented an eight per cent month-on-month (m-o-m) decline and a seven per cent year-on-year (y-o-y) decrease.

Data from the Malaysian Palm Oil Board (MPOB) showed CPO production in Sabah, Malaysia’s biggest palm-growing state slumped 21 per cent last February.

The lower production was partly due to seasonal factor and the lagged effects of the 2015-2016 El Nino phenomenon which has affected fresh fruit bunches (FFB) yields.

Correspondingly, CPO exports in February at 1.09 million MT, signaled a decline of 15 per cent m-o-m and 12 per cent y-o-y as well as weaker domestic consumption which fell 22 per cent m-o-m and dropped 31 per cent y-o-y to 0.16 million MT.

Analysts observed the lower m-o-m exports figures was due to reduced demand as majority of the major importing countries such as China, India, US, Pakistan were importing less.

China, for instance imported 53,000 MT of CPO in February 2016, a sharp decrease of 49 per cent m-o-m and a contraction of 18 per cent y-o-y, a reflection of the economic slowdown in the country.

Meanwhile, renowned palm oil expert, Dorab Mistry said Malaysia’s palm oil production will continue to head south as a result of the effect of stronger than expected El Nino.

“This El Nino is doing what all big El Ninos do – lowering production and boosting prices. I shall not be surprised if the deficit for first half 2016 as compared with first half 2015 will be in excess of 1 million tonnes,” he was reportedly said last week.

He believed the El Nino effect will continue to add pressure on CPO production and forecasted production will decline by 2 million MT in the year through September.

At the same time, analysts observed the FFB yield in February has reached record low.

The research arm of TA Securities Holdings Bhd (TA Research) in a recent report said due to the effect from the dry weather coupled with the seasonal low production period, FFB yield in Malaysia was only 0.99 tonne per hectare (ha), the lowest yield on record.

TA Research noted FFB yield in Sabah dropped by 0.24 percentage points to 0.94 tonne per ha while in Sarawak, it stood at 0.89 tonne per ha.

On another note, the research firm noted Peninsular Malaysia recorded some improvement as the FFB yield increased slightly from 1.01 tonne per ha to 1.07 tonne per ha in February.

Thus, the research firm opined the below average yield will persist throughout the year as El Nino effect has kicked in.

Similarly, Malaysian palm oil stockpiles slided to an eight-month low of 2.17 million tonnes in February.

Mistry added, “World stocks will be drawn down dramatically. We are already seeing this happen in palm oil in Malaysia and will see this soon happen in Indonesia.

“Stocks in consuming countries like India and China will also thin down,” he predicts.

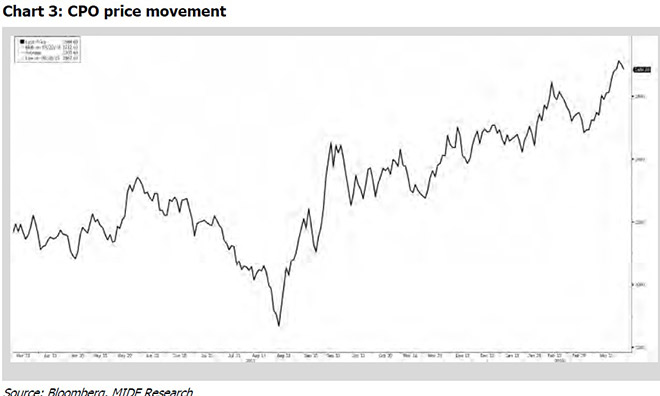

CPO price on an uptrend

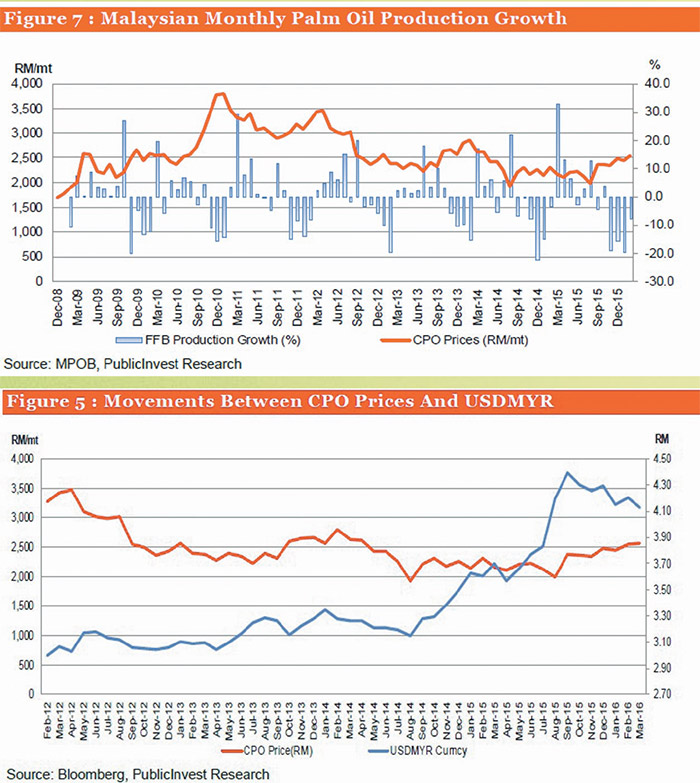

With the twin effects of lower palm oil production and declining inventories, CPO prices had been steadily rising over the past few months.

The Malaysian palm oil futures rose to a two-year high on March 28 with the contract for June delivery on Bursa Malaysia Derivatives Exchange reached RM2,758 per tonne.

Crude palm oil futures (FCPO) touched a high of RM2,764 per tonne on the same day, a level last seen since March 21, 2014.

Analysts and industry players sounded more bullish on the CPO price movement and believed the price still has more room to climb higher.

Mistry for instance has forecasted the CPO price to hit RM3,000 per MT on lower output.

“I believe we must now cast aside all ideas of CPO futures at RM2,600 or RM 2,700 (per MT).

“We have to take prices to levels where demand does not expand and is made to shrink somewhat in price-sensitive markets like India.

That will mean … futures trading with a three rather than a two,” he was quoted as saying during a conference in Kuala Lumpur recently.

In sync with the seasonal market observer, the research arm of MIDF Amanah Investment Bank Bhd (MIDF Research) has upgraded its CPO price forecast for 2016 to RM2,450 per MT from RM2,300 per MT previously.

MIDF Research analyst Alan Lim in a report dated March 25 said the reasons for the increase in CPO price assumption were severe stockpile depletion in the second quarter of 2016 (2Q16), the US potentially producing less soybean that earlier estimate and low crude oil price which is not expected to affect CPO price movement.

He said, “Malaysia palm oil stockpile is expected to drop to the critical level of 1.5 million MT towards the end of 2Q16.

“The impact of El Nino on oil palm tree production is only at the beginning stage.

“Hence, CPO production will be significantly lower than what is used to be in the first half of 2016 (1H16).

“We think that there is a chance that the CPO discount against soybean oil should narrow even to zero level due to severe supply shock in the market.

“Such rare phenomenon occurs before in Feb 2011 in which CPO price surge to RM3,800 per MT as inventory drop to 1.48 million MT,” he opined.

Lim noted globally the US Department of Agriculture has also estimated lower soybean production at 320.21 million MT.

He believed the forecast should be positive to CPO price as lower soybean production should lead to lower competition from soybean oil towards CPO.

Apart from that, Lim observed there is little correlation between Brent crude oil and CPO price movement when the former fell below US$80 per barrel in November 2014.

Therefore, he opined crude oil price movement should not affect CPO price unless it surges above US$80 per barrel as the price level should be the breakeven point for biodiesel players to start producing independent of government subsidy.

Similarly, crude palm kernel oil prices had also jumped the most in five years on March 28 on worries of lower output which could limit supplies in Malaysia.

Palm oil futures traders opined production of palm kernel oil, along with CPO could be affected by the El Nino conditions.

They believed El Nino which has also impacted the output of coconut oil, a substitute of CPO has contributed to higher demand for palm kernel oil, which in turn led to an increase in price.

Rejuvenating biodiesel programme

Rising CPO prices have definitely provided an impetus for the country to implement the B10 biodiesel programme this year.

Plantation Industries and Commodities Minister Datuk Amar Douglas Uggah Embas is confident that the country can implement the programme which can provide a wider usage for the economy.

He was reportedly said the plantation industries and commodities ministry was undertaking consultations with all the stakeholders to ensure the acceptance of the policy that will be carried out.

“Some testing needed to be done and final discussion will be carried out to make sure the implementation will be as smooth as possible.

“For us, we feel that B10 is sufficient at the moment in view of our stock and cost involved.

“As far as facilities are concern, Malaysia has set up an efficient system which can blend the new biodiesel within two days,” Uggah revealed recently.

He disclosed in January that the government is committed to reduce carbon dioxide emissions in the country by using biodiesel.

Apart from that, the B10 programme could also contribute towards the country’s economic growth.

Malaysian Biodiesel Association deputy president U. R Unnithan believed with higher consumption of palm biodiesel under the B10 programme at 1.2 million tonnes a year, it is anticipated to help lower palm oil stock by 600,000 tonnes annually and increased CPO price by about RM680 per tonne.

“The potential impact on gross domestic product (GDP) by B10 would be RM13.6 billion on account of CPO price alone.

“This would be about 25 per cent higher compared with the impact by the current B7 programme.

“We feel the B10 programme is a right step towards increasing its contribution to Malaysia’s GDP,” he said.

‘Minimal impact from CPO export tax’

For the month of April, a five per cent export duty will be charged to plantation players in particular upstream players for their CPO exports.

Nevertheless, analysts foresee little impact on the export tax for planters and CPO price movement.

CIMB Research, the investment arm of CIMB Investment Bank Bhd in a report said the export tax will be slightly negative for Malaysian pure planters like Hap Seng Plantations Holdings Bhd and Genting Plantations Bhd which could receive lower domestic prices for CPO.

However, the research firm believed it will be a boon for downstream players such as Wilmar International Ltd which would enjoy higher processing profit margins due to the differential between the higher export tax on CPO against refined palm products.

Concurring with CIMB Research, the research division of Public Investment Bank Bhd (PublicInvest Research) in another report said the wider tax gap between crude and refined palm oil will give refiners some incentives to ramp up utilisation rate, which had fallen below 50 per cent year-to-date.

“We believe the refinery utilisation rate will likely improve to at least 70 per cent in the coming months due to the re-introduction of CPO export duty.

“Local oleochemical and specialty fats producers should also benefit from the competitive prices as (profit) margins improved.

“Currently, processed palm oil makes up 66 per cent of our total CPO exports,” the research firm said.

Besides, PublicInvest Research also believed the upstream players will channel their CPO production to local refineries to avoid paying the CPO export duty.

It explained that the export tax should help to increase palm oil refining activities and refiners’ profit margins as more CPO supplies will flow into refineries before being exported overseas.

Furthermore, it opined the five per cent export duty will lead to about RM125 per MT cut on CPO price for Malaysian upstream players.

That, in turn, the research firm believed will provide a more level playing field between local and Indonesian palm oil refiners.

PublicInvest Research estimated that based on the additional margin of RM125 per MT for local refiners, it would narrow the differential profit margin between Malaysian and Indonesian refiners closer to about RM15 per MT or less, down from about RM40 per MT.

Given a more competitive pricing, the research firm believed processed CPO export volume should increase with downstream players regaining their market shares.

In anticipation of improved export volumes as well as weaker production in the coming months, PublicInvest Research believed CPO prices would fare better this year.

The research firm expects CPO prices to trade above RM2,800 per MT once inventories fall below 2 million MT psychological level.

Prospects for Sarawakian planters

Locally, plantation players which include Jaya Tiasa Holdings Bhd (Jaya Tiasa), Ta Ann Holdings Bhd (Ta Ann), Sarawak Oil Palms Bhd (SOP) and Rimbunan Sawit Bhd (Rimbunan Sawit) are expected to benefit from the recovery of CPO prices.

Their earnings for upcoming quarters are poised to improve due to higher realised average selling prices of CPO and crude palm kernel as a result of the positive sentiment surrounding the movement of the CPO price.

In particular, Jaya Tiasa and Ta Ann which have diversified earnings contribution from timber and oil palm plantation are set to maintain their favourable financial performances going forward.

Both companies had in last year benefitted from the exports of logs due to firmer prices on the international market attributed to shortage of logs supplies.

Jaya Tiasa in latest quarterly financial results announcement noted the current low palm oil stock level coupled with the effect of El Nino as well as the expected implementation of the biodiesel B10 mandate by Malaysian Biodiesel Association should stabilise the demand and prices of CPO.

Hence, the company remains optimistic about the long term prospects for the palm oil industry.

Jaya Tiasa’s chairman Tan Sri Abdul Rahman Abdul Hamid in the company’s annual report said, “We will continue to improve our oil extraction rate (OER) from CPO mill operation by imposing stringent control over operation efficiency and FFB input quality.

“With further fine tuning, we expect production volume and efficiency to improve in the financial year ending June 2016.

“As at June 30, 2015, the weighted average of our palm age is still below seven years.

“We expect our FFB yield MT per hectare to continue to improve and consequently reducing our cost of production.

“We will endeavour to lower our cost of production by enhancing our harvesting yield and productivity so that we are poised to reap the profits in the event CPO prices start to trend upwards.

“Our palm trees have a relatively young age profile. FFB yield will improve as more trees mature to their prime,” he believed.

He added the company’s additional CPO mills will boost its CPO production while expanding vertical integration should contribute positively to the palm oil division in the current financial year ending June 2016.

With those measures and advantages, Abdul Rahman said the group plans for a steady long-term growth and will ensure the company is well prepared for a recovery.

On another note, he believed prices for timber products especially logs are expected to remain firm due to the restricted supply and the robust demand from importing countries.

He is optimistic that the company’s financial year 2016 (FY16) ending June will continue to be a profitable year for its timber division.

AmInvestment Bank Bhd (AmInvestment Bank) in a research note earlier this year said Jaya Tiasa’s FFB yield was on recovery path after the group achieved just 12.5 tonnes per mature hectare for FY15 ended June 2015 due to labour shortage that led to the neglect of about 10,000 hectares of planted area.

The research firm believed the company is on track to meet its FFB production projection of 900,000 tonnes for FY16.

At the same time, AmInvestment Bank raised its FY16 earnings estimate for Jaya Tiasa by about 11 per cent to account for higher CPO price.

Moving on to another planter, Ta Ann, its chairman Datuk Amar Abdul Hamed Sepawi believed the company’s palm oil division will be the main driver for the group’s earnings growth for the year.

He observed with the anticipated recovery of palm oil price, higher revenue contribution is expected from the palm oil division. Abdul Hamed foresees the group’s FFB production is expected to rise further as the company’s young oil palm plantation estates gradually matures.

He noted FFB production from the group’s oil palm estates increased by 12 per cent last year.

Abdul Hamed stressed that the group’s focus this year will be in cost management, enhancing operational efficiency, increasing productivity and revising operational and marketing strategies to accommodate the changing operating environment and shifting of buyers’ preferences.

The research arm of Maybank Investment Bank Bhd (Maybank IB Research) in a report dated March 2 said Ta Ann’s strong FFB production will continue to drive its earnings growth by leveraging on its young oil palm plantation.

In the near term, the research firm believed the company’s earnings upside will emanate from an El Nino induced CPO price rally in 1H16 to boost earnings and further weakening of the ringgit against the US dollar to boost its timber earnings.

Interestingly, Ta Ann was reported to have partner with SOP to assist in developing the oil palm industry in Sarawak through a tie-up with MPOB.

AmInvestment Bank in a report dated March 11 said MPOB has agreed in principle to take the lead in research to improve oil palm yields in Sarawak.

The research firm believed the development is positive for Ta Ann, adding that other plantation players in Sarawak should join in as well in undertaking the industry wide measures.

Looking ahead, AmInvestment Bank said Ta Ann’s prospects in plantation look bright with FFB production targeted to grow at 15 per cent annually over the next three years.

Moreover, SOP believed the performance of the group would continue to be driven by palm products price movement which is dependent on the world edible oil market, movement of the ringgit and economic situation.

RHB Research said SOP’s production could surprise on the upside in the early stages of drought as Sarawak is typically plagued by more rain, which depressed yield.

The research firm had in a report last year raised its earnings estimate for SOP on the account of higher average CPO price.

As for Rimbunan Sawit, the company will focus on cost management and operational efficiency while expects the CPO price to maintain its upside trend for the coming quarter in view of the El Nino impact.

However, the company believed with global consumption remain soft in view of the Chinese economy slowdown while the supply of soybean continued to increase, the situation might alleviate further uptrend in CPO price.

To round it up, the bullish sentiment surrounding the plantation industry caused by the greater impact of drought which fueled CPO price rally is not going to end soon.

There might be more room for CPO price to trade higher in the coming months as palm oil stockpiles decline.

Many analysts expect CPO prices to remain firm and to some extent rally throughout 2016.

Therefore, plantation stocks could be in for a good time and possibly going through a re-rating in the near future.