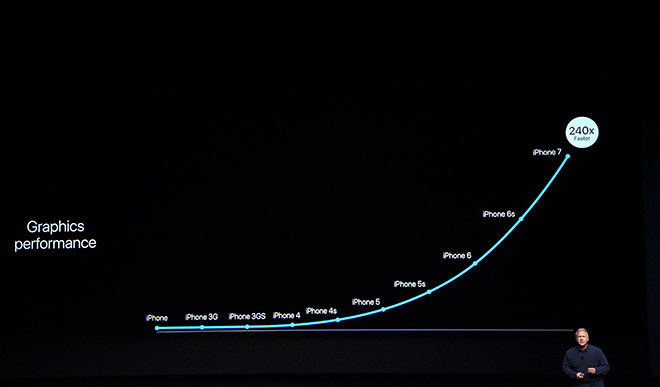

The launch of iPhone 7 and iPhone 7 Plus recently was greeted with overwhelming response, being sold out online even before hitting the stores worldwide.

The launch of iPhone 7 and iPhone 7 Plus recently was greeted with overwhelming response, being sold out online even before hitting the stores worldwide.

Many fans of Apple Inc’s (Apple) products were seen queuing up in front of Apple stores to be the first to grab the smartphone with enhanced features such as improved camera, no headphone jack and a water resistant body.

As the US-based technology company prepared for the launch of its next smartphone during its 10th anniversary in 2017 which could be iPhone 8, could semiconductor chipmakers – including suppliers – potentially benefit from more orders in the coming months?

The iPhone 8 is rumoured to have a glass body with a radical design that include an edge-to-edge display, eliminating the top and bottom of the smartphone’s outside frame.

With a complete makeover, the display screen will maximise the interface area of the new smartphone and is poised to be using flexible organic light-emitting diode (OLED) as compared to liquid crystal display (LCD).

Industry players outlined that OLED displays provides amongst others better viewing angles, greater power efficiency to maximise battery life and a faster response time than an LCD for faster refresh rates.

Besides, iPhone 8, a premium model of the next smartphone by Apple could be without the Home button while sensors such as Touch ID and front-facing camera would be fitted in the display.

Market observers noted that Apple had been working on developing touch and display driver integration (TDDI) chips since 2015 and thus, iPhone 8 could be one of the first new device to be using the new technology.

Internally, the iPhone 8 is poised to be installed with 10-nanometre A11 chip processor that would be faster and more efficient.

Apple is also said to be seeking a supplier for wireless charging chips that could enable its smartphone to be charged using long-range wireless charging technology.

Other than that, Apple is predicted to consider using advanced biometric features in its upcoming smartphone models such as facial recognition or iris scanning.

Hence, with more advanced features to be incorporated towards the development of Apple’s next smartphone and other devices, semiconductors players and those along the supply chain might benefit from higher sales orders.

In addition to Apple, other smartphone manufacturers like Samsung Electronics Ltd, Huawei Technologies Co. Ltd and LG Electronics Inc are also believed to be lining up new models of new smartphones for launching next year to fight for market share.

As manufacturers are gearing up for their next devices to hit the market next year, those supplying inputs for instance semiconductor chips, processors, sensors as well as wireless components could be in for a good run.

Locally, those companies include Globetronics Technology Bhd (Globetronics), Inari Amertron Bhd (Inari), Unisem (M) Bhd (Unisem) and Malaysian Pacific Industries Bhd (MPI) and so forth.

Could semiconductors players benefit from more orders?

The increasing demand for innovative technology products by consumers have pushed the production of smart devices such as smartphones to include more features and functions.

Besides smartphones, market observers believed catalysts for the growth of the semiconductor industry include the development of smart devices and electronic components for the healthcare and automotive industries.

For the automotive industry, a huge number of semiconductors components particularly sensors, processors and chips are required especially the talk of the town to bring self-driving cars into reality.

The demand for chips, telematics and connectivity and advanced driver assistance systems (ADAS) are envisaged to grow on a double-digits growth rate.

Locally, KESM Industries Bhd (KESM) which specialises in electronic manufacturing services (EMS) and provides semiconductor burn-in services, electrical testing of semiconductor integrated circuit (IC), tape and reel assembly has been tipped to benefit from rising automotive sales and increased electronic chips content in cars.

Affin Hwang Investment Bank Bhd (Affin Hwang) in a report dated August 15 said KESM provides a good proxy to the stable and growing automotive semiconductor segment.

The research firm believed KESM is in the right segment to benefit from an automotive structural growth story with strong growing demand for electronics for vehicles, from safety to infotainment and autonomous vehicles.

It noted KESM is an approved vendor for most automotive integrated device manufacturers (IDM) adding that more than 70 per cent of the company’s revenue in financial year 2015 was derived from the automotive segment.

Citing semiconductor market research firm IC Insights, Affin Hwang said the automotive segment would be the fastest growing sub-segment within the semiconductor industry.

The research firm opined that the healthy growth in the automotive segment would be spurred by the production of autonomous vehicles.

An autonomous car is basically a vehicle that is capable of sensing its environment and navigating without human input and uses a variety of techniques such as radar, lidar, global positioning system, odometry and computer vision.

Affin Hwang noted the autonomous vehicle market is expected to grow to US$41 billion by 2025 and thus could result for the increase of electronic components in vehicle given higher vehicle sophistication.

The research firm believed the growth should result from the increase of electronic components in vehicle given more sophistication in vehicle design including safety features.

It observed that one key areas, vehicle infotainment, which includes navigation is another growth impetus for the automotive segment.

For the longer term, Affin Hwang opined that the growth in the automotive segment for KESM will be positive.

Similarly, the research arm of Kenanga Investment Bank Bhd (Kenanga Research) in a report dated August 9 noted KESM is at the forefront of emerging technologies development.

The research firm said KESM is well-positioned to capitalise on the trend following the success of the company’s development of proprietary process control for the test during burn-in (TDBI) for vehicle which could identify how, when and where devices or equipment might fail.

Thus, the research firm believed KESM is poised to benefit from cost efficiencies in the future.

Moreover, Kenanga Research noted automotive manufacturers are exploring ways to TDBI their products in line with the growing need to meet stringent quality requirements and productivity gains for a new generation of chips.

TDBI is a testing process using high temperatures and critical testing patterns to accelerate the defective failures of integrated circuits.

KESM’s executive chairman and chief executive officer (CEO) Sam Lim in a statement recently said: “We are just at the starting point of an exciting road ahead focusing on our strategic plans.

“Our customers are rolling out new devices and solutions to meet the growing demands by the car makers.

“We see great potentials as increasing new automotive devices are required for added features in the evolution of cars and our opportunities will remain as the demand grows,” Lim said during the company’s financial year 2016 (FY16) ended July 2016 results announcement on September 20.

Demand for the company’s burn-in and test services of automotive chips was particularly strong in FY16, he said.

For FY16, KESM revealed that the group’s revenue grew by nine per cent year-on-year (y-o-y) to RM285.73 million while net profit jumped by 46 per cent y-o-y to RM30.68 million as compared with FY15.

Looking ahead, Lim believed KESM is superbly positioned in its target market and remains confident going into 2017 with great optimism.

Other players on the fast track

Moving on, another semiconductor manufacturer which has exposure to the automotive industry is MPI.

AllianceDBS Research Sdn Bhd (AllianceDBS Research) in a report said the automotive segment made up 24 per cent of the revenue of MPI group in FY16 ended June 2016.

Despite MPI’s exposure in the automotive segment, the largest contributor to the group’s revenue is still the smartphone or tablet segment.

Following a company’s briefing on the outlook for FY17, AllianceDBS Research said the company expects sales to be modest as demand remained soft especially for the smartphone segment.

In spite of that, the research firm expects the company to record slightly better earnings in FY17 attributed to weaker ringgit as sales are denominated in the US dollar.

Apart from that, other semiconductor players which manufacture equipment for the automotive sector include Vitrox Corporation Bhd (Vitrox), MMS Ventures Bhd (MMS Ventures) and Elsoft Research Bhd (Elsoft).

Vitrox’s products from its automated board inspection (ABI) segment were being utilised by its automotive customers.

Vitrox’s CEO Chu Jenn Weng in the company’s annual report said: “Despite the anticipated moderate grow or decline in the semiconductor capital equipment spending in 2016, we firmly believe that the demand for automation and machine vision inspection systems in the semiconductor and electronics assembly manufacturing sectors will grow further due to the miniaturisation of electronics products and rapid changes in the consumer electronics and gadgets.

“Furthermore, in the near future, everything will be connected, everything will be mobile and everything will be measured, driving the need for better infrastructure; efficient data management and analysis and ubiquitous access to cloud services.

“With a broader product offering, wider global market presence coupled with strong collaboration between major outsourcing semiconductor assembly ans test (OSAT) and electronics manufacturing services (EMS) companies, strategic channel partners and internal sales and support teams, we believe our core business will grow in tandem with the development of the semiconductor and electronic manufacturing industries in 2016.

“The key ABI growth initiative in 2016 will be to support or to enable our customers in the ‘Industrial Internet of Things’ (IIoT) transformation,

“We will be promoting this turnkey solution to the global market aggressively in 2016 in order to support and enable our customers’ transformation into the new era of smart manufacturing,” he said.

Affin Hwang noted that Vitrox has seen increasing orders for the vision inspection equipment from the automotive and data server industries.

The research firm observed both segments currently accounted for more than 30 per cent of Vitrox’s revenue and were being driven by new customers as the company’s equipment penetrated new markets.

Likewise, the research arm of Maybank Investment Bank Bhd (Maybank IB Research) in a recent report said Vitrox is making good progress for the company’s new inroad into the wafer or non-tech inspection equipment market.

The research firm gathered that by the end of 3Q16, Vitrox would have delivered one wafer inspection equipment and one robotics advanced 3D optical inspection (AOI) for the inspection of precision fabricated parts (customised for automotive and consumer electronics industry).

Besides that, Maybank IB Research believed there would be some interesting transitions for Vitrox in 2017 as the company is moving to a bigger manufacturing plant that could cater for more orders and enable the company to increase production.

The research firm noted Vitrox’s business remained healthy as represented by the three-month average book-to-bill ratio which stood at 1.11 times as at end of July 2016 while strong backlog order could sustain the company’s revenue in the second half of 2016.

For MMS Ventures and Elsoft, Affin Hwang said the stronger revenue growth of both companies in 2Q16 which soared by 76 per cent and 240 per cent respectively have been driven by the automotive and smartphone segments.

The research firm pointed out that both companies are direct competitors within the light-emitting diode (LED) testing equipment space and also in the supply chain for a leading smartphone manufacturer.

It believed a surge in new equipment orders, for the upcoming replacement model of a new smartphone could have contributed to their recent strong performance in 2Q16.

The research firm gathered that both companies could expect strong performances in the coming quarter should there be strong take-up for the new smartphone.

Aside from that, Inari, a semiconductor manufacturer which provides testing services and acts as a contract manufacturer for US-based Broadcom Corporation (Broadcom) is likely to gain from more orders.

AllianceDBS Research in a report said Broadcom, one of Inari’s key customers and top radio frequency chipmakers in the world is in the midst of increasing the radio frequency (RF) filters capacity (by converting six-inch wafer to eight-inch wafer fab) which should ease supply constraints.

The research firm added the benefit would allow Broadcom to supply to other smartphone manufacturers in the future besides Apple and Samsung.

The research firm expects demand for Broadcom’s RF content in smartphones to continue to grow rapidly in the medium term driven by rising adoption of 4G Long Term Evolution (LTE), smartphone variant consolidation and further integration of RF modules.

It outlined that rising LTE adoption will drive Broadcom’s growth and in turn Inari’s as Broadcom is the dominant supplier of high-band frequency RF products due to the company’s superior film bulk acoustic resonator (FBAR) filters.

AllianceDBS Research gathered that Broadcom’s current FBAR production is on an allocation basis to the company’s main customers while demand continues to be more than supply.

As a result, it noted Broadcom is doubling the company’s FBAR filter capacity which is likely to be completed by 3Q16.

Owing to Broadcom’s expansion, AllianceDBS Research said Inari also needs to expand the manufacturing capacity to meet the increase in RF sales volumes from Broadcom.

Meanwhile, it observed that Inari has started ramping up operations for the company’s new testing division, Inari Integrated System (IIS).

AllianceDBS Research believed the new testing division could drive Inari’s next leg of growth.

The research firm noted the new testing division was to meet the demand of the company’s key customers.

It gathered IIS will cater to the testing of network chips where demand is stable.

It opined revenue from the new testing division would help to support the seasonality in Inari’s earnings once contribution from IIS becomes more substantial in the future.

AllianceDBS Research also believed significant content gains in latest smartphone models especially Apple’s iPhone would help to meet its 30 per cent growth forecast for Inari’s RF segment in FY17 ending June 2017.

The research firm noted Inari’s medium term outlook seems to be relatively secure due to Broadcom’s three-year supply agreement with Apple until 2018.

AllianceDBS Research foresees bright outlook for Inari over the medium term given positive sentiment for the sales of new iPhone model in 2017 where a major design overhaul is expected.

At the same time, Affin Hwang was also upbeat about Inari’s outlook as it remains optimistic on the company’s RF operations and opined that the company is well positioned for a potentially exponential growth in the fibre optics segment.

The research firm believed LTE adoption (and the eventual transition from 4G to 5G) will continue to raise RF content per device driving growth despite an overall slowdown in smartphone sales, while a take-off in Internet of Thing (IOT) should accelerate the demand for Inari’s fibre optic products.

Other catalysts for the semiconductor industries include wider usage of wearable devices and emerging market trends such as the IOT, big data and artificial intelligence that demand.

With that, manufacturers will produce gadgets that provide more functions, powerful and user-friendly.

A tepid year for semiconductors

While technology and electronic companies were focusing on the smartphone market this year, the semiconductor industry at large was clouded by a muted outlook.

The World Semiconductor Trade Statistics (WSTS) had forecasts global sales of semiconductor components to decline

by 3.2 per cent to US$325 billion in 2016.

Nonetheless, the organisation believed sales is expected to rebound next year with a growth of two per cent to US$331 billion in 2017.

Subsequently, it opined that the industry will resume its growth with an increase of 2.2 per cent in 2018 to US$338 billion.

In the meantime, WSTS noted the largest growth this year is expected to be derived from sensors, discrete seminconductors components and analog products with the largest declines expected in memory and optoelectronics.

Going forward, the organisation believed all major product categories and regions except logic are forecasts to return to growth in 2017 under a stable economic environment.

Concurring with WSTS are US-based research and advisory firm providing information technology related insight Gartner Inc (Gartner) and International Data Corporation (IDC) which believed the industry could fell into a contraction this year.

They observed the subdued outlook was attributed to the global server market in which revenues have shown y-o-y decline.

Gartner cited variations of growth by data centre segments and exchange rate issues were the cause of the decline while IDC believed sluggish investment in hyperscale data centre and tough y-o-y comparisons as a result of th Intel Corporation INTC led enteprise refresh cycle were the reasons for the dismal performance.

Also contributed to the dismay performance of the industry was the lower sales of chips in particular for personal computers amidst weaker demand which still made up a portion of the semiconductor industry.

An analyst observed weaker demand for certain semiconductor components has driven manufacturers to hold back in increasing production in the near term.

Nevertheless, he foresees demand to recover in the second half of 2016 buoyed by improving economic environment.

A local research firm, TA Research was also bullish on the semiconductor sector.

The research arm of TA Securities Holdings Bhd observed that bookings activity has picked up while billings remained strong at 13.1 per cent y-o-y and 9.6 per cent y-o-y last July.

It opined that semiconductor companies under its coverage were generally expecting a better performance in the coming quarter supported by demand from Chinese firms.

The research firm gathered that Unisem and MPI believed their sales would stay flat or slightly up in the coming quarter.

Moreover, it noted Inari expects the company’s radio frequency (RF) utilisation rates to recover to 80-85 per cent in third quarter of 2016.

Generally, TA Research continued to be positive on the semiconductor sector on expectations of a better second half coupled with the weak ringgit which could boost revenue as a result of foreign exchange sales.

Opportunities exist despite slower smartphone growth

Despite the slowdown in sales in the smartphone industry, TA Research believed there are still opportunities for growth in that segment of the semiconductor sector.

The research firm in a report dated September 23 said the smartphone industry remains one of the fastest growing segments, driven by smartphone adoption in emerging markets.

In emerging markets, TA Research said smartphone sales is expected to be driven by first time buyers as they convert from feature phones to smartphones, aided by the increasing affordability of smartphones.

The research firm pointed out that a particular country of interest is India.

It observed that smartphone ownership in the country remained low at 17 per cent despite being the world’s second largest populated country.

TA Research noted 78 per cent of individuals in India are still using feature phones out of the people that own a cellphone.

Therefore, the research firm believed India is widely tipped to become the second largest smartphone market by value over the next few years.

It opined that there are also opportunities for companies to outpace the industry through market share gains within Chinese vendors and higher RF content within smartphones.

TA Research also believed semiconductor manufacturers can also capitalise on growing smartphone content to fuel their growth.

It noted RF content is expected to benefit from the growth in LTE devices and advent of carrier aggregation.

Owing to that, the research firm gathered the value of RF content in a premium 4G smartphone is estimated to be 20 times more than the value within a legacy 2G or 3G smartphone.

Citing research by US-based semiconductor company, Qorvo, TA Research noted the RF total addressable market (TAM) is estimated to grow at a compound annual growth rate (CAGR) of 15 per cent between 2014 and 2018.

The research firm noted Inari, MPI and Unisem are primary involved in the production of RF components.

On another note, it opined that better than expected initial demand for iPhone 7 could potentially bode well for smartphone sales in the second half of 2016.

The research firm also believed sales of smartphone should also be supported by the weak ringgit environment in which it expects to continue on account of potential US interest rate hikes by year end.