Malaysian palm oil futures rebounded and closed at 2,634 as market underpinned by weaker ringgit while traders cover their position ahead of public holiday.

Malaysian palm oil futures rebounded and closed at 2,634 as market underpinned by weaker ringgit while traders cover their position ahead of public holiday.

Crude palm oil futures (FCPO) benchmark December 2016 contract settled at 2,636 on Friday, down 40 points or 1.5 per cent from 2,676 last Friday.

Trading volume decreased to 203,882 contracts from 213,345 contracts from last Monday to Thursday.

Open interest based decreased to 760,617 contracts from 770,554 contracts from last Monday to Thursday.

Intertek Testing Services (ITS) reported that exports of Malaysia’s palm oil products during September fell 15 per cent to 1.378 million tonnes compared with 1.621 million tonnes during August.

Socete Generale de Surveillance’s (SGS) report showed that Malaysia’s palm oil exports during September fell 15.8 per cent to 1.366 million tonnes compared with 1.621 million tonnes during August.

Overall, demand significantly decreased from India, China and Europe Union. Spot ringgit fell and weakening to 4.1320 as worries about Deutsche Bank soured risk sentiment offset support from higher oil prices.

India announced that it would lower its import duty on crude palm oil and refined vegetable oils by five per centage points to 7.5 per cent and 15 per cent, respectively, as part of efforts to curb food inflation.

The Organization of the Petroleum Exporting Countries (OPEC) agreed on Wednesday to cut output to 32.5 to 33 million barrels per day (bpd) from around 33.5 million bpd.

On Monday, the price rose and hit a five-month after cut in India import duty on crude palm oil and supported by weaker ringgit.

On Tuesday, the price slid from five-month high on Tuesday as weaker-performing rival oils weighed on market sentiment and profit taking.

On Wednesday, crude palm oil market fell and recorded sharpest daily decline in six weeks as weaker-performing rival oils continue to weigh on market sentiment.

On Thursday, the price rose and rebounded from two-week lows as stronger energy market boost the market sentiment despite gains seems capped by weaker export outlook.

On Friday, the price rose on Friday as weaker ringgit underpinned the price while traders cover their position ahead of public holiday.

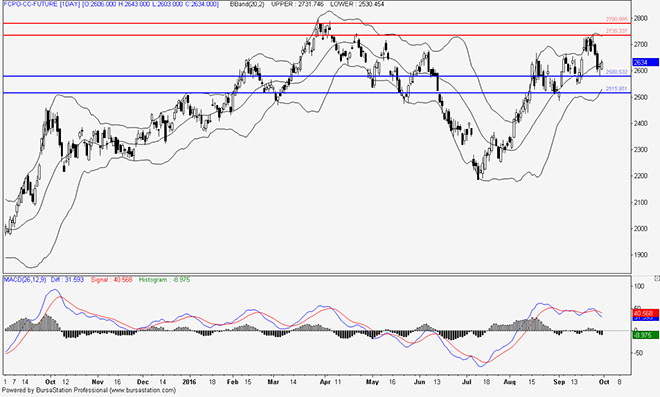

Technical analysis

According to the weekly FCPO chart, the price opened higher as MACD remained stay above zero line which could signal that continuation of current uptrend.

By the end of the week, Bollinger Bands showed expanding sign which could indicate an increase in price momentum.

On Monday, price rose while market test and under pressure by the upper Bollinger Band. MACD showed a potential divergence which should be monitored closely to confirm sustainability for current uptrend.

On Tuesday, the price fell and market continue to approach middle Bollinger Band. MACD continue to show a potential divergence sign which should be monitored closely to confirm sustainability for current uptrend.

On Wednesday, the price fell and closed below the middle Bollinger Band. MACD showed bearish crossover above zero line and formed divergence sign which could indicate that current price may relatively weak in short term.

On Thursday, the price test and limited by the middle Bollinger Band. MACD showed bearish crossover above zero line and formed divergence sign which could indicate that current uptrend movement may remained under pressure.

A daily doji candlestick could provide indecision signal for next market direction in short term.

On Friday, the price rose and rebounded after a daily doji candlestick while middle Bollinger Band could provide further indication on next market direction in short term.

In the coming week, the price has potential to range between 2,735 and 2,550. Resistance lines will be placed at 2,735 and 2,780, support lines will be positioned at 2,550 and 2,515, these levels will be observed in the coming week.

Major fundamental news this coming week

MPOB, ITS and SGS report released on October 10 (Monday).

Oriental Pacific Futures (OPF) is a Trading Participant and Clearing Participant of Bursa Malaysia Derivatives. You may reach us at www.opf.com.my. Disclaimer: This article is written for general information only. The writers, publishers and OPF will not be held liable for any damage or trading losses that result from the use of this article.