Malaysian palm oil futures fell for first session in three at 2,869 on Friday as tracking weaker performing rival oils market while market continue underpinned by a weaker ringgit.

Malaysian palm oil futures fell for first session in three at 2,869 on Friday as tracking weaker performing rival oils market while market continue underpinned by a weaker ringgit.

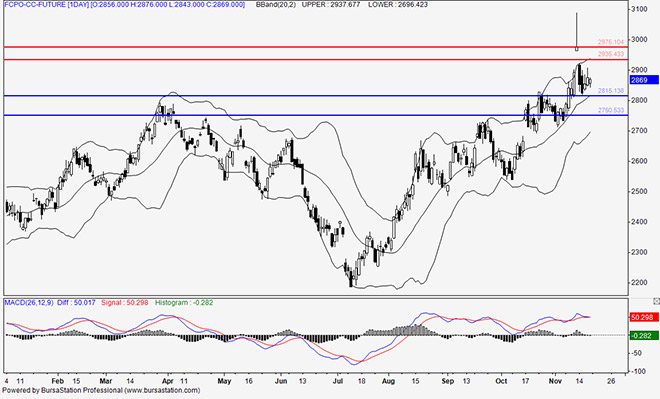

Crude palm oil futures (FCPO) benchmark February 2016 contract settled at 2,869 on Friday, down 95 points or 3.2 per cent from 2,964 last Friday.

Trading volume increased to 218,437 contracts from 168,168 contracts from last Monday to Thursday.

Open interest based decreased to 783,590 contracts from 829,584 contracts from last Monday to Thursday.

Intertek Testing Services (ITS) reported that exports of Malaysia’s palm oil products during November 1 to 15 fell 17 per cent to 520,870 tonnes compared with 627,864 tonnes during October 1 to 15.

Socete Generale de Surveillance’s (SGS) report showed that Malaysia’s palm oil exports during November 1 to 15 fell 19 per cent to 513,745 tonnes compared with 633,252 tonnes during October 1 to 15.

Overall, demand weakened simultaneously from European Union, India and China. Spot ringgit slid to a fresh 11-month low of 4.41 against the dollar on Friday as the ringgit has become Asia’s worst performing currency, after Donald Trump’s surprising win in the US presidential election sparked a global sell-off in emerging markets.

According to a circular on the Malaysian Palm Oil Board website on Tuesday, Malaysia will lower its crude palm oil export tax to six per cent in December, down from 6.5 per cent in November.

Reuters’s survey showed that Indonesia’s crude palm oil (CPO) output likely rose for a sixth month in October while exports were seen rising as buyers build up inventories.

On Monday, the market posted biggest fall in over four months as profit taking and tracking weaker performing rival oil markets.

On Tuesday, the price fell for second consecutive day as weaker demand expectation weighed on the palm oil market.

On Wednesday, the price rose for the first time in three sessions as tracking oversea vegetable oil markets gains.

On Thursday, the crude palm oil market rose for second consecutive day on Thursday as supported by a weaker ringgit and stronger performing rival oil market.

On Friday, the price dropped as tracking rival oil market losses while market remained underpinned by a weaker ringgit.

Technical analysis

According to the weekly FCPO chart, weekly candlestick opened lower as current market retraced back from the upper Bollinger Band and stay away from overbought condition. By the end of the week, the upper and middle Bollinger Band continue heading upward which could signal that current uptrend could remained in long term.

On Monday, the price fell as market retraced back from the upper Bollinger Band and stayed away from overbought condition. A bearish ‘abandon baby’ candlestick pattern potentially provide uptrend correction signal in short term.

On Tuesday, the price fell as market continue approaching the middle Bollinger Band which could potential provide significant support for the current market in short term. MACD remained stayed above zero line which could indicate that current uptrend momentum could remain in long term.

On Wednesday and Thursday, the price rose as the Bollinger Bands continued heading upward which could indicate that continuation of current uptrend in long term.

MACD potentially showed bearish crossover above zero line and indicate that current price significant weak in short term while current uptrend momentum could remain in long term.

On Friday, the price fell as MACD continued to show bearish crossover above zero which indicate that current price remained significant weak in short term. Next week, the price has potential to range between 2,935 and 2,750.

Resistance lines will be placed at 2,975 and 2,935, support lines will be positioned at 2,815 and 2,750, these levels will be observed in the coming week.

Major fundamental news this coming week

ITS and SGS report released on November 21 (Monday).

Oriental Pacific Futures (OPF) is a Trading Participant and Clearing Participant of Bursa Malaysia Derivatives. You may reach us at www.opf.com.my. Disclaimer: This article is written for general information only. The writers, publishers and OPF will not be held liable for any damage or trading losses that result from the use of this article.