Malaysian palm oil futures held near their strongest level in four and a half years at 3,158, supported by weaker ringgit and tight supplies while gains were capped by profit taking. Crude palm oil futures (FCPO) benchmark March 2016 contract settled at 3,161 on Friday, drop 113 points or 3.7 per cent from 3,048 last Friday.

Malaysian palm oil futures held near their strongest level in four and a half years at 3,158, supported by weaker ringgit and tight supplies while gains were capped by profit taking. Crude palm oil futures (FCPO) benchmark March 2016 contract settled at 3,161 on Friday, drop 113 points or 3.7 per cent from 3,048 last Friday.

Trading volume increased to 177,627 contracts from 170,499 contracts from last Monday to Thursday.

Open interest based increased to 754,352 contracts from 746,838 contracts from last Monday to Thursday.

Intertek Testing Services (ITS) reported that exports of Malaysia’s palm oil products during December 1 to 15 fell 7.6 per cent to 481,349 tonnes compared with 520,870 tonnes during November 1 to 15.

Socete Generale de Surveillance’s (SGS) report showed that Malaysia’s palm oil exports during December 1 to 15 fell 9.6 per cent to 464,582 tonnes compared with 514,745 tonnes during November 1 to 15.

Overall, demand strengthened from Europe and China, while demand remained weak from India. Spot ringgit slumped to a 14-month low at 4.4755 on Friday after the US Federal Reserve surprised markets by indicating an early rate hike next year.

Indonesian Palm Oil Association (GAPKI) said in a statement on Tuesday that Indonesia’s exports of palm oil and palm kernel oil in October rose nearly 40 per cent to 2.41 million tonnes from a month earlier.

Industry regulator MPOB data showed on Wednesday that oil inventories in Malaysia climbed to their highest levels in four months at end-November, but were still below forecasts due to a sharper than expected drop in production.

MPOB data showed that production fell 6.1 per cent from a month earlier to 1.57 million tonnes, the lowest level since July, with the harvest disrupted by year-end monsoon rains.

On Monday, Bursa Malaysia Derivatives market closed due to public holiday, Birthday of Prophet Muhammad.

On Tuesday, the market ended three losing sessions and rose as market underpinned by lower output expectation.

On Wednesday, the market rose for a second consecutive session as the market, supported by industry regulator, showed lower output and stock compared with the market’s expectations.

On Thursday, crude palm oil market rose and hit a four and a half year high, underpinned by weaker ringgit and tight supplies which boost market bullish sentiment.

On Friday, the market held near their strongest level in four and a half years, supported by weaker ringgit and tight supplies while gains were capped by profit taking.

Technical analysis

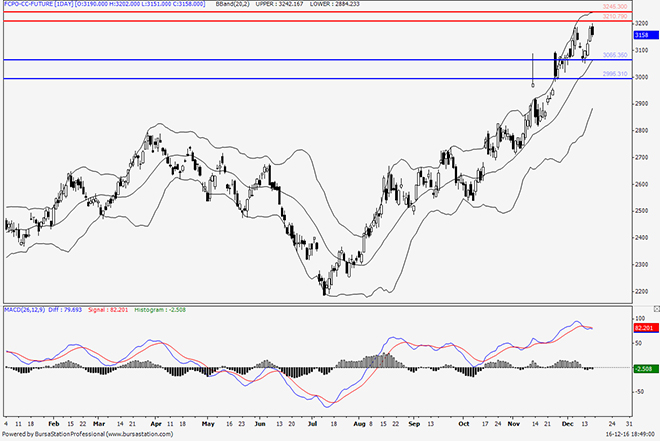

According to the weekly FCPO chart, weekly candlestick rose and attempted to test the upper Bollinger Band. By the end of the week, market closed below the upper band and remained under pressure by the upper Bollinger Band. Both Bollinger Bands continued heading upward which could indicate that the current uptrend could remain in long term.

On Monday, Bursa Malaysia Derivatives market closed due to public holiday, Birthday of Prophet Muhammad.

On Tuesday, the price rose as the Bollinger Bands continued heading upward which could indicate that the current uptrend could remain in the long term.

On Wednesday and Thursday, the price rose as market continue approach the upper Bollinger Band while a daily bullish ‘Marubozu’ could provide bullish indication in the short term.

On Friday, the market declined as the upper Bollinger Band started to show signs of stagnation while MACD potentially showed less bullish crossover above zero line which could provide price correction signal in the short term.

In the coming week, the price has potential to range between 3,245 and 3,065. Resistance lines will be placed at 3,210 and 3,245, support lines will be positioned at 3,065 and 2,995, these levels will be observed in the coming week.

Major fundamental news this coming week

ITS and SGS report released on December 20 (Tuesday).

Oriental Pacific Futures (OPF) is a Trading Participant and Clearing Participant of Bursa Malaysia Derivatives. You may reach us at www.opf.com.my. Disclaimer: This article is written for general information only. The writers, publishers and OPF will not be held liable for any damage or trading losses that result from the use of this article.