“We are going to fix our inner cities, rebuild our highways, bridges, tunnels, airports, schools, hospitals; we are going to rebuild our infrastructure which will become, by the way, second to none. And we will put millions of our people to work as we rebuild it,” proclaimed US president-elect Donald J Trump, during his victory speech following his surprise landslide victory in the recent US presidential elections.

“We are going to fix our inner cities, rebuild our highways, bridges, tunnels, airports, schools, hospitals; we are going to rebuild our infrastructure which will become, by the way, second to none. And we will put millions of our people to work as we rebuild it,” proclaimed US president-elect Donald J Trump, during his victory speech following his surprise landslide victory in the recent US presidential elections.

It has been a year and a half since the official launch of Trump’s presidential campaign, and since then, media outlets around the world have been hanging off Trump’s every word, hoping to catch another outrageous claim or comment made by the future US president which has led to his campaign rhetoric being widely publicised the world over.

Disregarding the purely outrageous and controversial claims previously made by Trump, his campaign has been premised mostly on promises of increases in infrastructure spending, tax cuts and protectionists policies such as the non-pursuit of the Trans-Pacific Partnership Agreement (TPPA).

Following this, Trump’s victory has led to large spikes in US dollar gains against most ASEAN currencies as investors are now more confident in US-denominated assets and the US market. The Malaysian ringgit, in particular, has been observed to be among one of the most affected emerging market currencies.

Moreover, with the US’s current status as one of the main partnering countries for Malaysia exports, coupled with the fact that Malaysia has enjoyed an average trade to GDP ratio of 148 per cent from 2010 to 2015, Trump’s policies will be a huge determinant to our trade market and, in turn, our overall economic growth and health.

While Trump’s victory has not really affected Malaysia’s economy in real analytics as no new policy will be announced until after his official inauguration, indirectly, the shock victory has led to increased depreciation of the ringgit and waning investor confidence.

The rising US dollar

Currently, US infrastructure is graded a D+ by its very own American Society of Civil Engineers (ASCE), and estimated to require US$3.6 trillion to upgrade by 2020.

As such, Trump’s emphasis on infrastructure spending in particular has been said to be a huge contributor to his victory as American voters were swayed by the promises of rebuilding the countries’ crumbling infrastructure while providing accelerated economic growth and productivity gains.

In an analysis of proposed infrastructure spendings of presidential candidates, by Peter Navarro and Wilbur Ross, senior policy advisors to the Trump campaign, the duo explained that Trump’s plan to encourage US$1 trillion in private sector infrastructure spending via US$140 billion in tax credits – or 82 per cent of the quality amount – for infrastructure construction investing companies, would be growth-inducing.

“It would cut taxes, reduce regulations, remove restrictions on energy development and eliminate our debilitating trade deficit. As growth rapidly accelerated, Trumpnomics would generate millions of additional jobs and trillions of dollars in additional income and tax revenue,” cited a recent Washington Post article authored by Navarro and Ross.

In addition, the tax cuts are expected to lower the cost of financing for the projects to the tune of 18 to 20 per cent by effectively reducing the equity component through the tax credit which will, in turn, reduce the revenues needed to service the financing and improve the project’s feasibility.

Investors seem to be rather swayed by such bold forecasts as they anticipate Trumponomics to increase return rates of US markets and US dollar denominated assets.

This is reflected by the observed rally in US stocks and benchmark US treasury yields surging sharply, and an estimated US$2.4 billion that flowed out of emerging market stocks and bonds, in the first week following Trump’s victory.

Jameel Ahmad, vice president of Corporate Development and Market Research at Forex Time (FXTM), explains this phenomenon: “Investors have basically bought into the mindset that Donald Trump will introduce business-friendly policies into the US economy and this has encouraged an increased sentiment towards the US with the promise of fiscal stimulus likely to lead to a bounce higher in US economic growth.

“This has consequently also increased the US interest rate outlook and resulted in investors being driven towards the US dollar.”

In turn, as investors are now keener on the prospect of higher less risky returns on treasury yields, and the explosive potential of US’s infrastructure segment, this has not only badly affected emerging market companies’ ability to service dollar-denominated debt but also emerging market currencies and, in particular, Malaysia’s currency has been among the hardest hit – touching a low of 4.4785 per US dollar, the lowest in almost 19 years.

The plunging ringgit

In response to the rapidly plunging ringgit, Bank Negara Malaysia (BNM) has brought out several measures that are expected to broaden the domestic foreign exchange (forex) market to improve liquidity and depth of the onshore market, and, in turn, support the ringgit in the immediate term.

“Overall, the announced measures are intended to promote a deeper, more transparent and well-functioning onshore forex market where genuine investors and market participants can effectively manage their market risks with greater flexibility to hedge on the onshore market,” shared Vincent Loo, an economist with RHB Research Institute Sdn Bhd (RHB Research).

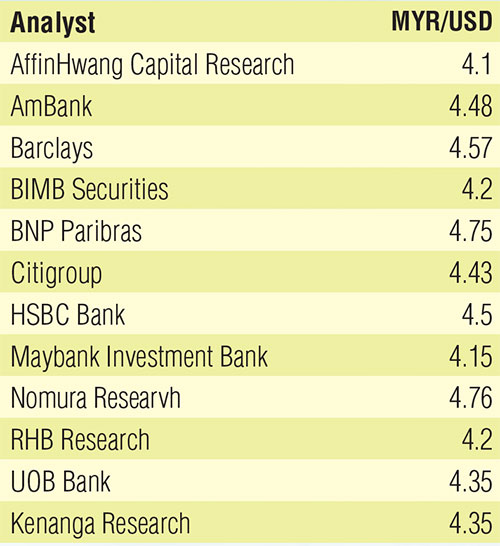

Ringgit outlook for end-2017 // Source: BT and Bloomberg

While the volatility of the ringgit has reduced since the implementation of these measures, it is undeniable the ringgit is still on a declining trend, and as we watch our ringgit continue to weaken against the US dollar with abated breath, the question on everyone’s lips at the moment is why is the ringgit plunging?

To answer this question, Jameel asserts that “the ringgit is being heavily pressured by consistent and renewed strength in the US dollar and this has been the theme of the global markets since the unexpected outcome to the US election.”

“The movements in the ringgit are not based on news about the local economy but are being directed by the market fluctuations and extreme buying sentiment towards the US dollar. All currencies are facing the same amount of pressure and even the Japanese yen has weakened by over 12 per cent in the past month against the US dollar.”

Jameel continued on to explain while BNM’s measures are likely to achieve the goal of improving domestic demand for the ringgit at least in the short term, in the longer term, they are unlikely to be key drivers as the US dollar will dictate upcoming directions in the ringgit as it has done in the past.

“Over the longer term, all emerging market currencies and even developed currencies like the Euro will be trading in response to the US dollar. As such, the Trump inauguration in late January is seen as a major event risk as the reaction that ensues could make or break the current US dollar buying frenzy.

“If Trump indicates it will take time for his reforms to be passed through the system, the temptation to take profit on the US dollar is going to be strong and this would be positive towards the global currencies reversing their losses over the final period of 2016.”

However, with Trump’s inauguration still weeks away, the future of US policies or Trumponomics is still very much up in the air and only time will tell what direction these policies will take. Of course, even without the effects of Trump’s inauguration, there are still other factors pressuring our ringgit.

Looking beyond the recent plunge of the ringgit, the local currency has already been on a steady declining trend for the most of 2016 with a recorded steep 8.0425 per cent year over year (y-o-y) decrease on November 7, the day before Trump’s election victory.

Dar Wong, chief investment strategist for Dektos Investment Corp, conjectures that the ringgit devaluation in 2016 was mainly due to falling crude oil prices and political complications, causing investor’s confidence to wane and pull out their funds from Malaysia.

However, there seems to be a possible change to this as Wan Suhaimie Saidie, head of economic research of Kenanga Investment Bank Bhd, shares that in the medium-to-long term, BNM’s measures which will lead to the strengthening of the onshore ringgit and re-duction of the volatility in the ringgit forex, are expected to help enhance confidence in the Malaysian economy towards foreign and domestic investors alike.

Waning confidence

Unfortunately, it may be a while before we actually see restored confidence in the Malaysian economy as investors fret about uncertainties of a global economic recovery due to the known unknowns of the upcoming Trump presidency, the outcome of the upcoming Brexit referendum, rising populist movements, and fears of China overheating.

One specific known unknown of a Trump presidency that has left investors skittish about Malaysia’s economy specifically is Trump’s anti-trade rhetoric and campaign promises to withdraw from the TPPA, a free trade agreement between 12 countries, to which Malaysia is a party to.

Suhaimie believed that if Trump were to follow-through with his anti-trade rhetoric, “it will limit the potential upsides from the nascent recovery of global demand, and will place greater strain on the domestic sector as a driver of Malaysia’s economic growth.”

He further explained that, due to Malaysia’s participation in the TPPA, a potential US withdrawal from it would be a signal of growing anti-trade sentiments between the US and Malaysia which might impede recovery in Malaysia’s external sector and, in turn, our economy on the whole.

Additionally, a lack of US participation may cause the TPPA to fall through completely and among participants within the TPPA, the US, Japan and Singapore are major importing partners to Malaysia exports, taking up between 30 to 35 per cent of the total local exports.

According to Wong, mathematically, this will send an impact to Malaysia’s trade economy.

However, it is still early days to assume the fate of the TPPA, and regardless of the outcome, it is seems Malaysia will remain an attractive destination for companies from the US.

During an interview with The Borneo Post, acting Deputy Chief of Mission of the US Embassy, Edgard D Kagan shared this view, saying the US would remain committed to the entire Asian pacific region due to heavy economic interests at stake within the region.

Kagan defended his view, citing that “the proof of that is how many American companies have significant presence here in Malaysia (over 600 companies). There is obviously the Oil and Gas (O&G) sector, the electrical and electronic (E&E) industries – and also a variety of other industries, consumer goods, and services, and recent years has seen more and more American companies coming to Malaysia.

“American companies have done Greenfield investments, they’ve expanded existing facilities, and some of them have moved their regional headquarters to Malaysia. I think all of that reflects a great deal of confidence in Malaysia,” he concluded.

Suhaimie agrees, noting that even with Trump’s rhetoric of returning jobs to Malaysia, it is unlikely to shift US Foreign Direct Investments (FDI) away from Malaysia due to cost consi-deration.

“Indeed, given Malaysia’s relatively strong economic fundamentals, we believe it is better positioned than its emerging market counter-parts in curbing these outflows,” he said.

Wong, however, is of a less optimistic opinion, remarking that Trump’s blatant anti-Islamic stance will more or less affect all Islamic countries, including Malaysia, when measuring the FDI.

As it is unlikely Trump will change his sarcasm on many world issues, Wong advises that Malaysia should find new opportunities and look towards leaning on China and ASEAN trade partners instead for business viability.

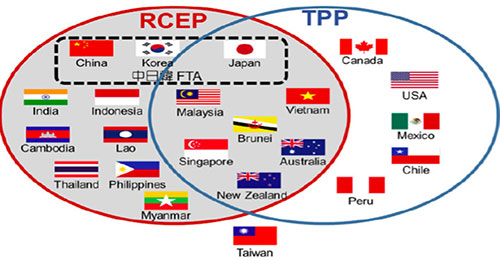

Regional Comprehensive Economic Partnership

One potential alternative to the TTPA is the Regional Comprehensive Economic Partnership (RCEP), a proposed free trade agreement (FTA) between all Asean countries, and six coun-tries that possess existing FTAs with an Asean country.

“In my opinion, RCEP involves 16 countries and could replace the TPPA for sure,” opined Wong, adding that the involvement of all Asean countries and majority economies of Asia and Australasia, will allow the RCEP to be a more smoothening trade tie compared to the TPPA.

The inclusion of China in particular seems to be a major point for the RCEP as Wong notes that due to China’s immense population and regional location to Malaysia, the RCEP would be hugely beneficial to Malaysia’s regional economic growth with such a large potential con-sumer demand.

“Moving into the next decade, we hope to see the expansion of market demand from India and other emerging markets in Asia like the Philippines and Indonesia,” Wong said.

On the other hand, Suhaimie believed the success of the RCEP to Malaysia would largely be dependent on how Malaysia positions itself to benefit from China’s rising middle class and how it will tap its growing demand.

Future outlook of ringgit

Looking forward, Jameel opines that it is still far too early to provide a fair estimation or prediction on the ringgit’s performance in the coming year, as there is much speculation on whether Trump will actually be able to implement his campaigned policies as soon as he gets inaugurated.

A delay in their implementations could reverse the fortunes of the US dollar but conversely this means the dollar could get even stronger if Trump’s promises are fulfilled, leading to increased pressure on the ringgit.

According to Jameel, another factor to watch out for will be the US interest rate expectation for 2017. He explains that as financial markets are now expecting the Federal Reserve to raise US interest rates three times next year, emerging markets will face a threat of readjustment when it comes to capital outflow if these predictions are accurate.

The predictions are beginning to run true as showcased by the US interest rate hike of 25 basis points earlier this month — from 0.50 to 0.75 per cent by the US Federal Reserve.

On the other hand, Wong, as a registered fund manager in Singapore, with 28 years of experience in global financial investment and trading industry, shares his expertise and predicts that prices will find support while some sectors might recover fast, indicating tailwinds for the ringgit.

“Theoretically, the US dollar -ringgit is well resisted at 4.60 though it is heavily guarded at 4.50 regions at the moment. A potential improvement in political and economic climate will push the ringgit stronger back to 4.10 levels. This outlook is valid till June 2017 and the second half will depend on a more fundamental study,” he opined.

Taking a more cautious approach, Suhaimie forecasts that the ringgit will strengthen slightly in 2017 to 4.35 from the estimated 4.45 at the end of 2016 due to an anticipated reversal in US dollar strength.

“Furthermore, assuming a stronger than expected rebound in oil prices (exceeding the US$55 per barrel mark), we may expect to see further strengthening of the ringgit to around 4.25,” Suhaimie shared.